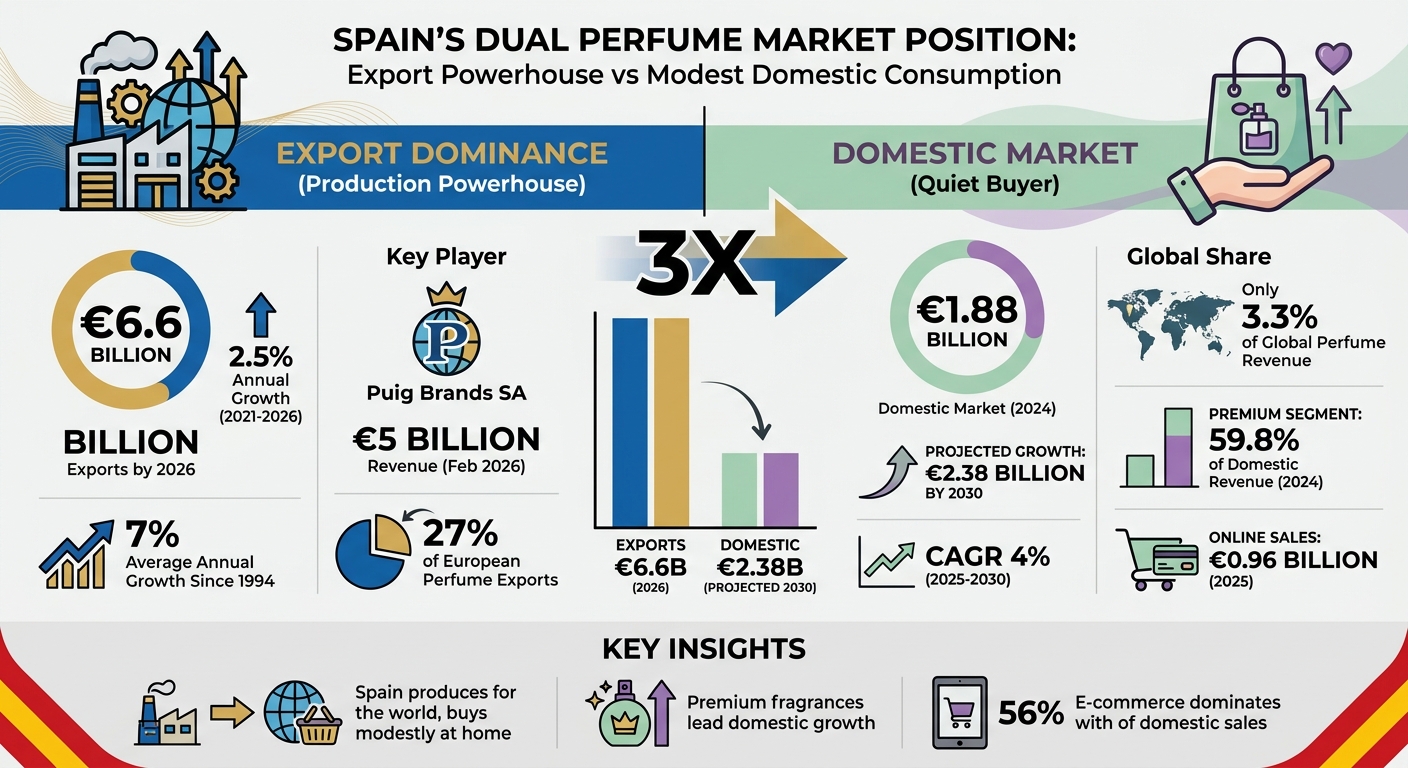

Spain is a global leader in perfume production and export, yet its domestic consumption remains modest. By 2026, exports are projected to reach €6.6 billion, nearly three times the domestic market value of €1.88 billion in 2024. Spain’s strength lies in its high-quality essential oils and premium fragrances, with brands like Puig driving €5 billion in revenue. Domestically, the market is shifting towards luxury fragrances, expected to grow at a 4% CAGR, reaching €2.38 billion by 2030. Online sales dominate, contributing €0.96 billion in 2025, while tourism significantly boosts premium segment sales. Challenges include rising costs, stricter regulations, and evolving consumer preferences.

Spain Perfume Market: Export vs Domestic Revenue 2024-2030

Spain’s Production Dominance

Spain has carved out a strong position in the fragrance industry, particularly in manufacturing and exports. At the heart of this success is Puig Brands SA, a major player headquartered in Barcelona (Plaza Europa, L’Hospitalet de Llobregat). By early 2026, Puig had achieved an impressive revenue milestone of €5 billion, cementing its place among global leaders in the industry. This robust production capability directly supports Spain’s export ambitions, which are outlined below.

27% Share of European Perfume Exports

Spain’s cosmetics and perfume exports are on a steady growth trajectory, projected to rise from €5.6 billion in 2021 to €6.6 billion by 2026. This represents an average annual growth rate of 2.5%, underpinned by a production infrastructure that has expanded at an average rate of 7% per year since 1994. These figures position Spain as a critical supplier in Europe, with strong export ties to markets like France, Italy, and Germany.

Rather than competing on sheer volume, Spanish manufacturers focus on crafting high-value fragrances. This strategy allows them to maintain healthy profit margins while keeping their domestic footprint relatively modest. Such export strength lays the groundwork for understanding Puig’s global impact.

Puig Portfolio and Global Market Reach

Puig’s influence extends well beyond Spain, with a portfolio of globally recognized brands that cater to premium consumers. However, forecasts from February 2026 hint at a potential slowdown in the fragrance sector. This shift highlights the need for agility as consumer preferences evolve, moving away from single "signature scents" toward owning multiple fragrances tailored to different moods or seasons.

Spanish manufacturers, including Puig, are responding by focusing on high-quality formulations. For instance, fragrances with higher oil concentrations that offer up to 12 hours of longevity are becoming increasingly popular, aligning with the global trend toward premium products. To stay ahead, companies are also integrating cutting-edge technologies like AI and augmented reality (AR) for faster product development and virtual scent trials.

Raw Materials and Supply Chain

Spain’s Mediterranean climate provides a distinct advantage for cultivating essential perfume ingredients such as orange, jasmine, and various citrus fruits. This local abundance reduces the need for imports and strengthens Spain’s position as a vertically integrated producer. Regions like Andalusia and Catalonia are experiencing a resurgence in artisanal perfumery, blending traditional craftsmanship with sustainable practices like green chemistry and upcycling to create eco-friendly ingredients. The use of 100% organic alcohol and recycled glass has become a standard in production, meeting the growing consumer demand for "clean" luxury. These efforts not only improve product quality but also enhance Spain’s reputation as a reliable supplier on the global stage.

Despite its focus on local cultivation, Spain’s demand for cosmetics imports has grown by 4.4% annually since 1994, highlighting an active and well-integrated supply chain. By balancing local resources with strategic imports, Spanish manufacturers ensure efficient production while scaling to meet international demand.

Domestic Market Trends and Growth

Spanish consumers, despite strong domestic production, contributed just 3.3% of global perfume revenue in 2024. The domestic market itself generated €1,880.3 million that year, with forecasts projecting growth to €2,381.1 million by 2030, reflecting a moderate 4% compound annual growth rate (CAGR). This shift in consumer behaviour highlights intriguing trends in revenue, product preferences, and buying habits.

Market Size and Revenue Projections to 2030

Spain’s perfume market reached €1.71 billion in 2025, climbing from €1,470.86 million the previous year. Analysts predict a steady CAGR of 5.48% to 5.56% through the early 2030s, with the market potentially hitting €2.79 billion by 2034. Among product categories, Eau de Parfum led the way in 2025, contributing €0.77 billion to the total market. This dominance stems from a growing preference for fragrances with higher oil concentrations and longer-lasting effects. Interestingly, personal use accounted for €1.04 billion of the market, highlighting a trend where Spanish consumers view fragrances as daily essentials rather than occasional gifts. These patterns underline a notable evolution in how consumers approach and value perfumes.

Premium vs. Mass Market Segments

The premium segment is clearly the rising star, making up 59.8% of total revenue in 2024 and showing the fastest growth. By comparison, the mass market, valued at €0.97 billion in 2025, continues to grow but at a steadier, volume-driven pace. Spanish consumers are becoming increasingly selective, gravitating toward premium and artisanal fragrances. Features like high-quality ingredients, sustainable packaging, and long-lasting formulations are driving this preference. This shift also mirrors a broader move away from the idea of a single "signature scent" to curated fragrance wardrobes - collections tailored to different occasions, moods, or seasons. Notably, about 33.6% of Spanish consumers now seek unique or exclusive fragrance combinations, valuing individuality over mass-market appeal.

Consumer Behaviour and Purchasing Patterns

Spanish buyers stand out for their focus on sustainability and functionality in fragrance choices. Scents marketed as mood-enhancing, featuring ingredients like lavender, jasmine, and bergamot, are seeing a surge in demand for their stress-relieving properties. Online sales reached €0.96 billion in 2025, but brick-and-mortar stores - especially department stores and speciality shops - remain crucial for the sensory experience of testing fragrances before purchase. Eco-conscious packaging options, such as refillable stations and bottles made from recycled glass, are also gaining popularity among Spanish consumers. Additionally, travel retail and duty-free outlets continue to play a significant role, particularly in tourist-heavy areas where both locals and visitors contribute to sales.

Top Spanish — Portfolio Brands Driving Exports

Puig Brands and International Performance

Puig Brands SA, based in Barcelona at Plaza Europa 46-48, L’Hospitalet de Llobregat, reached an impressive €5 billion in revenue by February 2026. This milestone places Puig among global luxury leaders like LVMH, Chanel, and Hermès in the competitive fragrance market. However, after years of rapid growth, the company expects a slowdown in fragrance growth for the remainder of 2026.

Puig has carved a niche in premium products and high-growth categories. Men’s luxury fragrances are growing the fastest, but women’s fragrances still dominate, contributing 61.06% of luxury revenue in 2024. This success is strongly tied to Spain’s expanding premium fragrance segment. In 2024, premium fragrances made up 59.8% of Spain’s total perfume revenue, providing a solid base for Puig’s global ambitions.

Online sales have become a cornerstone of Puig’s international strategy. By combining digital platforms with traditional retail, Spanish brands like Puig are able to reach global audiences more effectively. This approach is particularly important for Eau de Parfum, which generated €0.77 billion in Spain’s domestic market in 2025 and remains the top revenue-generating product type.

Beyond Puig’s dominance, Spain’s export portfolio is enriched by smaller, artisan fragrance brands that bring diversity to the market.

Niche and Artisan Spanish Fragrances

While Puig leads in export volumes, smaller artisan perfume houses are gaining traction by meeting the growing demand for exclusive and distinctive scents. These niche brands thrive within Spain’s premium fragrance market, offering an alternative to mass-market products with their unique blends.

The niche fragrance sector is poised for significant growth. Revenues are forecasted to hit €2,381.1 million by 2030, with the overall perfume market expected to grow to €2.79 billion by 2034. Artisan brands focus on sustainable packaging, high-quality natural ingredients, and limited-edition collections, appealing to eco-conscious and authenticity-seeking consumers. While Puig dominates in scale, these smaller brands enhance Spain’s reputation for craftsmanship and creativity, particularly in European markets where artisanal quality is highly prized.

Channel Mix: Online vs. Offline Distribution

Spain’s perfume market showcases an intriguing shift in how fragrances reach consumers, blending strong export capabilities with premium domestic production. By 2025, the market hit €1.71 billion, with online channels grabbing €0.96 billion of that total. This marks a significant milestone: digital channels now account for more than half of Spain’s fragrance sales. The appeal? Convenience, competitive pricing, and the rise of dynamic online platforms. Younger buyers, especially Gen Z and Millennials, are driving this trend, often discovering new scents through social media platforms like TikTok.

E-commerce Growth and Market Drivers

The dominance of online sales, reaching €0.96 billion, highlights the growing preference for digital shopping. While globally e-commerce makes up about 30% of fragrance sales, Spain’s online penetration surpasses this average, setting it apart. Platforms like warehouse clubs and e-commerce giants are thriving, while traditional retailers face increasing pressure to adapt.

This strong online momentum is prompting physical retailers to rethink their strategies, focusing on how they can complement - not compete with - the digital boom.

Offline Retail: Performance and Challenges

Brick-and-mortar stores remain relevant, but they’re evolving to stay in the game. In 2024, department stores in Spain generated €662.03 million in revenue, leveraging experiential strategies to attract shoppers. Specialty stores, which account for 42.65% of global fragrance sales, offer something online platforms can’t: personalised consultations, expert guidance, and in-store features like scent customisation bars. Many of these stores are integrating digital tools, such as AI-driven scent quizzes and refillable fragrance stations, to combine convenience with a hands-on experience.

One major advantage of physical retail is trust. Online marketplaces, while convenient, have seen a rise in counterfeit and grey-market products. This makes in-person stores a safer bet for consumers seeking authenticity and exclusivity. Duty-free shops also play a unique role, offering travellers the chance to purchase fragrances without worrying about liquid restrictions.

Channel Performance Comparison

Comparing online and offline channels reveals how Spain’s approach differs from global trends. Worldwide, offline channels still led the market in 2025, commanding 67.0% of revenue. However, Spain bucks this trend, with online sales nearly matching traditional retail. Out of the €1.71 billion market, e-commerce accounted for €0.96 billion, showcasing a digital shift that contrasts sharply with global norms. Department stores globally held 32.8% of the perfume distribution market in 2025, but their influence in Spain seems weaker when compared to the surging e-commerce sector.

Looking ahead, Spain’s perfume market is expected to grow to €2,381.1 million by 2030. Online channels are projected to outpace offline growth, particularly for mass-market fragrances, which generated €0.97 billion in 2025, benefiting from fierce online price competition. Meanwhile, premium fragrances - holding a 59.8% market share in 2024 - still rely on physical stores to provide the high-touch, sensory experiences that justify their price tags. This dual-channel strategy - mass-market thriving online and premium fragrances anchored in physical retail - reflects Spain’s ability to balance artisanal quality with modern consumer demands.

Your Personal Fragrance Expert Awaits

Take our quick scent quiz to discover authentic designer and niche fragrances matched to your taste — explore them as 2–8ml decants and samples, so you can try each one before committing to a full bottle.

Find Your ScentTourism Impact on Domestic Perfume Sales

Spain’s thriving tourism industry plays a vital role in boosting domestic perfume sales, complementing the country’s growing online and offline retail strategies. As a top global travel destination, Spain has positioned itself as both a leading producer and a key market for luxury fragrances. For many international visitors, premium perfumes serve as elegant, travel-friendly souvenirs, making them a popular purchase during their stay. As Vincenzo Carrara, Founder of CARRARA Advisory, explains:

"Spain’s popularity as a travel destination and its international appeal make it an important market for luxury fragrance tourism, with tourists often purchasing high-end perfumes as souvenirs".

Tourist Spending and Revenue Contribution

Tourism has a noticeable impact on the luxury perfume segment in Spain. In 2024, the premium fragrance market recorded €673.6 million in revenue and is expected to account for 48% of the market share by 2025, up from 39% in 2018. This mirrors global trends, where travel retail contributes around 15% of total fragrance sales. Cities like Barcelona and Madrid benefit significantly from tourist spending, particularly through international airports, flagship stores, and specialty boutiques that offer immersive scent experiences.

Coastal regions like Andalusia and the Balearic Islands also see increased demand during the summer for light, citrus-based fragrances. Meanwhile, niche and artisan scents are gaining popularity among tourists seeking unique and curated products, aligning with the broader trend toward personalized fragrance experiences. These patterns highlight the seasonal dynamics and the role of tourism in shaping local perfume sales.

Seasonal Sales and Duty — Free Shopping

Duty-free shopping is another channel where tourism significantly influences perfume sales. Fragrances purchased after airport security are exempt from standard liquid restrictions, making them a convenient last-minute option for travelers. The tax benefits available in these settings also encourage purchases within the premium segment.

Brands are adopting creative methods to engage tourists in these environments. Airport pop-up shops showcase exclusive limited editions, and high-traffic areas feature interactive tools like digital scent quizzes, AI-driven recommendations, and custom engraving services. Travel-size formats, such as 5 ml atomizers and pocket-friendly bottles, are increasingly favored by tourists for their portability. Additionally, high-concentration formats like Parfum are outperforming broader market trends in travel retail, appealing to shoppers who value both quality and longevity. These strategies not only enhance immediate sales but also reflect the growing integration of digital and tactile retail experiences, underscoring the evolving dynamics of the fragrance market in tourism-driven contexts.

2030 Outlook and Market Projections

Spain’s perfume industry remains a global leader in production, with its domestic market showing steady, albeit modest, growth. By 2030, the domestic market is expected to reach 2,381.1 million EUR, growing at a 4% CAGR between 2025 and 2030. Meanwhile, exports are forecasted to hit 6.6 billion EUR by 2026, highlighting Spain’s strength as a manufacturing powerhouse. Despite this, domestic revenue will account for only about 3.3% of the global market. These figures provide a foundation for examining the key factors shaping the industry’s future.

Growth Drivers: Premium Scents and Innovative Ingredients

The premium fragrance segment continues to dominate, holding a 59.8% market share in 2024 and set to grow even faster through 2030. Exotic ingredients like vanilla, oud, and iris are reshaping high-end collections. For example, in October 2025, Loewe, a Spanish luxury brand, introduced a line of exclusive fragrances featuring Roasted Vanilla, Bittersweet Oud, and Iris Root to appeal to this niche market.

In addition to traditional offerings, the industry is branching into innovative areas like neuro-fragrances, which aim to reduce stress or improve focus. There’s also a growing emphasis on sustainability, with brands incorporating upcycled ingredients into biodegradable formulations to align with clean beauty standards.

Challenges: Rising Costs and Regulatory Pressures

While opportunities abound, the industry faces notable challenges. Stricter EU regulations, alongside rising production costs, have increased R&D expenses by up to 25%, particularly due to compliance with IFRA standards on allergens and synthetic components. Extreme weather events, such as droughts and floods, are also driving up the cost of essential raw materials like jasmine and citrus. To mitigate these issues, manufacturers are focusing on ethical supply chains and diversifying sourcing options.

On the consumer side, shifting preferences toward experiences rather than material goods may temper domestic demand. To stay competitive, brands are turning to AI-driven innovation and sustainable practices to capture evolving consumer interests.

Balancing Domestic Growth and Export Dominance

Export revenues are on track to reach 6.6 billion EUR by 2026 - nearly triple the domestic market’s value - underscoring Spain’s position as a key exporter. Locally, the premium segment continues to shine, holding a 59.8% market share. This dual dynamic highlights Spain’s unique role in the global fragrance landscape, where strong production capabilities contrast with a more cautious domestic consumer base.

Conclusion: Spain’s Dual Market Position

Spain stands out as a global manufacturing leader in the fragrance industry while maintaining a comparatively modest domestic market. Exports are projected to soar to €6.6 billion by 2026, nearly three times the domestic market’s anticipated value of €1.88 billion in 2024. This highlights Spain’s role as a production hub rather than a consumption-driven market, holding a 3.3% share of global revenue.

While smaller in scale, the domestic market is steadily growing. By 2030, it is expected to reach around €2.38 billion, with prestige fragrances - forecasted to account for 59.8% of revenue in 2024 - leading this growth. Additionally, the rising popularity of Mediterranean-inspired artisanal scents, featuring local ingredients like orange blossom and jasmine, presents opportunities for both domestic and export markets.

However, challenges such as stricter regulations, fluctuating raw material costs, trade restrictions, and currency instability could affect profitability. Addressing these issues while exploring opportunities in areas like sustainable packaging, AI-based personalization, and niche fragrance development will be essential for Spain to maintain its competitive position through 2030.

Spain’s established infrastructure, supported by key players like Puig Brands SA and production hubs in regions such as Andalusia and Catalonia, provides a strong foundation to adapt to changing consumer demands and regulatory landscapes. The supply chain’s consistent growth - averaging 7% annually since 1994 - further reinforces this resilience.

To sustain its export leadership while nurturing domestic demand, Spain must focus on premium offerings and digital innovation. With e-commerce expected to match the mass-market segment at €0.96 billion by 2025, online retail offers a clear path for growth. Combining sustainable practices with the preservation of artisanal traditions will be key to thriving in the dynamic global fragrance market.

FAQs

Why does Spain export so much perfume but buy relatively little at home?

Spain plays a significant role in the global perfume industry, exporting a substantial share thanks to its robust production capabilities. In fact, the country accounts for 27% of EU perfume exports, with prominent players like Puig driving this success. Despite this strong export performance, domestic consumption tells a different story. By 2025, Spain is projected to represent just 2.2% of the global perfume market.

This modest domestic demand could stem from various factors. Consumer preferences may lean toward other product categories, or the market might be nearing saturation. Additionally, higher prices within the domestic market compared to international offerings could also influence purchasing habits. Together, these elements paint a picture of a market that excels abroad while facing challenges at home.

What is driving Spain’s shift toward premium fragrances through 2030?

Spain is witnessing a notable move toward high-end fragrances, fueled by changing consumer tastes and a growing inclination toward luxury goods. This trend is shaped by several factors: an increasing appetite for premium and niche scents, the convenience of purchasing luxury fragrances online, and the impact of the country’s vibrant tourism industry. These elements are working together to drive consistent growth in the luxury perfume market, supported by shifts in consumer behavior and Spain’s robust production and export capabilities.

How do tourism and duty-free sales affect perfume demand in Spain?

Tourism and duty-free shopping play a key role in boosting perfume demand in Spain. Tourists often encounter luxury fragrances while traveling, making these products more accessible and appealing. Duty-free shops at airports and other travel hubs further encourage international purchases, allowing consumers to explore premium scents at competitive prices. Together, these factors not only increase sales but also broaden the customer base for high-end perfumes.