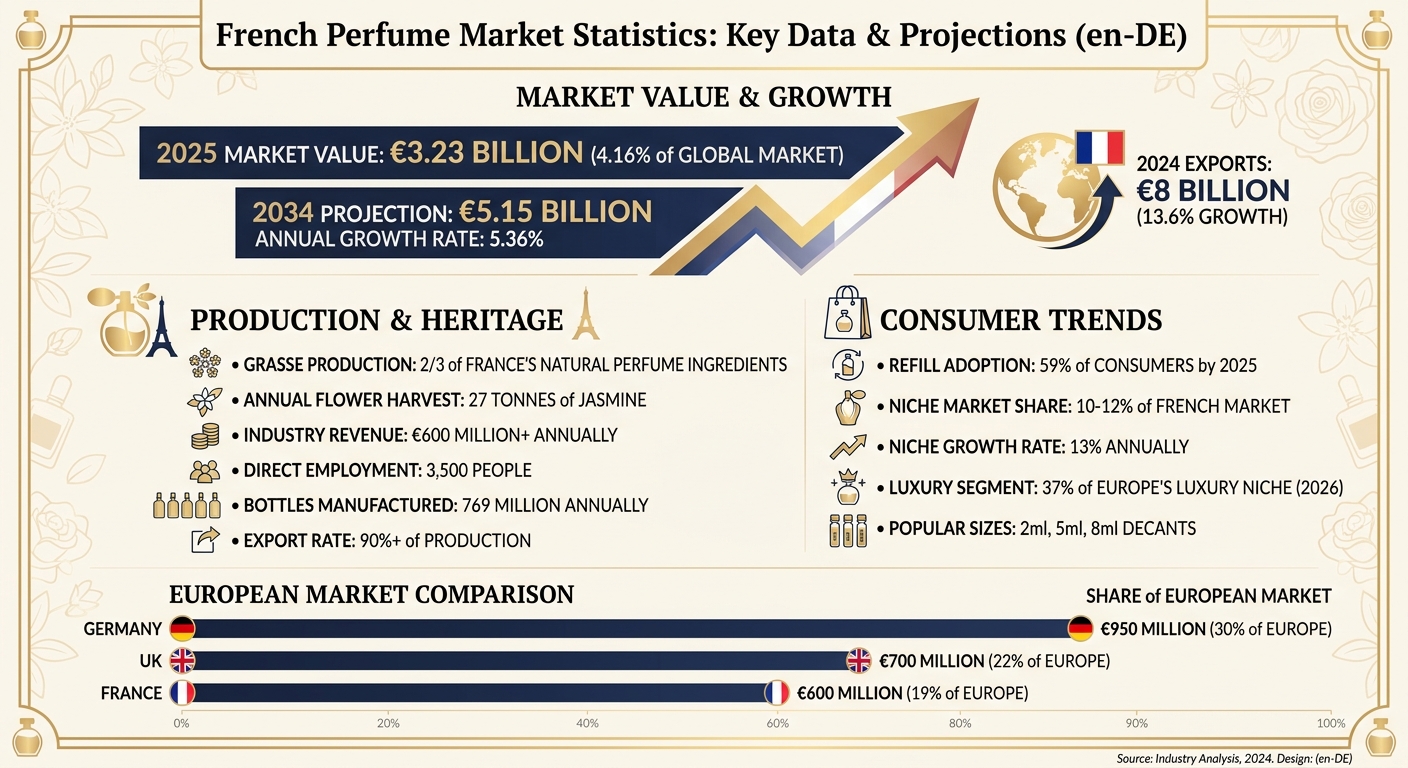

France remains the global leader in the perfume industry, driven by centuries of expertise and modern consumer trends. In 2025, the French perfume market was worth €3.23 billion, accounting for 4.16% of the global market. By 2034, this figure is set to grow to €5.15 billion, with a yearly growth rate of 5.36%. France also dominates exports, with €8 billion in sales in 2024, making it the largest exporter of luxury fragrances worldwide.

Key Highlights:

- Grasse: The historic perfume capital, recognized by UNESCO, produces over two-thirds of France’s natural perfume ingredients.

- Luxury dominance: France held 37% of Europe’s luxury niche segment in 2026, doubling the UK’s share.

- Consumer trends: French buyers now prefer smaller decant sizes (2 ml, 5 ml, 8 ml) and refillable bottles, with 59% opting for refills by 2025.

- Niche market growth: Growing at 13% annually, niche perfumes now make up 10–12% of the French market.

- Sustainability focus: Reduced glass bottle weight, refill systems, and bio-based ingredients are reshaping production.

The French perfume market blends historical craftsmanship with modern demands, ensuring its global influence continues to grow.

French Perfume Market Statistics 2025-2034: Growth, Exports & Consumer Trends

HOW FRANCE BECAME THE PERFUME CAPITAL OF THE WORLD? WATCH THIS BEFORE YOU BUY!

France’s Perfume Industry Origins

France’s dominance in the perfume world can be traced back to the 12th century in Grasse, where artisans first crafted scented leather goods to counteract the unpleasant smells of the tanning process.

The game-changer came in 1533 when Catherine de’ Medici introduced her personal perfumer to the French court. This sparked a craze for scented gloves, setting the stage for perfume to become a symbol of refinement. By 1614, the guild of glovers-perfumers was officially recognised by King Louis XIII, and in 1724, Grasse’s perfumers gained independence from tanners, marking the start of a dedicated fragrance industry. The 18th century saw perfume solidify its association with French luxury. Under Louis XV, the royal court earned the nickname "la cour parfumée", as perfume became essential for masking odours in an era when bathing was infrequent. Later, Marie Antoinette elevated perfumery further by commissioning complex floral blends from Jean — Louis Fargeon, including her famous Sillage de la Reine - a mix of tuberose, jasmine, orange blossom, and sandalwood.

These early innovations positioned Grasse as the epicentre of French perfumery and a global leader in fragrance production.

Grasse: Global Production Centre

In the 18th century, economic challenges pushed Grasse to adapt. The town’s unique microclimate - protected from coastal winds, warmed by inland air, and irrigated via the Siagne canal - created ideal conditions for cultivating aromatic plants. Grasse shifted from leather production to flower cultivation, with jasmine, rose, and tuberose becoming central to its economy.

By the late 19th century, around 65 companies in Grasse were processing raw materials, often sourced from French colonies, to meet rising global demand. The 1940s marked a peak, with the region producing 5,000 tonnes of flowers annually. Today, Grasse supplies over two-thirds of France’s natural aromas for perfumes and food flavourings, harvesting 27 tonnes of jasmine yearly. The local perfume industry generates over €600 million annually and directly employs 3,500 people, with an additional 10,000 working in related fields.

In 2018, UNESCO recognised Grasse’s perfumery expertise, highlighting its sustainable and traceable production methods. This acknowledgment has strengthened the region’s reputation, with luxury brands like Chanel, Dior, and Louis Vuitton forming partnerships with long-standing farming families to ensure high-quality, sustainable ingredients.

"We developed this very specific language and a culture of perfume that doesn’t exist in other places in the world." - Jacques Cavallier — Belletrud, Master Perfumer, Louis Vuitton

Cultural Impact on Perfume Development

France’s artistic heritage has profoundly shaped the global perception of luxury fragrance. By the 18th century, Grasse focused on raw material production, while Paris emerged as the hub for creating finished perfumes - a division that still defines the industry today.

Historic perfume houses reflect this cultural integration. Founded in 1747, Galimard is France’s oldest perfumery and once catered to the Royal Court. Molinard exemplified the fusion of fragrance and luxury by using Baccarat crystal and Lalique glass for its bottles. Chanel No. 5, crafted in Grasse by Ernest Beaux for Coco Chanel, revolutionised the industry with its use of aldehydes and reliance on locally grown jasmine and roses.

The industry now incorporates around 6,000 essential oils derived from flowers, fruits, resins, and even animal sources. Grasse remains a training ground for "les nez" (noses), experts who can identify over 2,000 scents. The Grasse Campus trains more than 800 students in chemistry and perfumery, ensuring the continuation of the expertise recognised by UNESCO. With France commanding roughly 30% of the global perfume market, its legacy of craftsmanship continues to shape modern perfumery.

The enduring influence of these traditions is evident in today’s market, where the blend of heritage and modern techniques meets consumer demand and sets industry standards.

Production vs. Consumption Analysis

Production Volume and Export Figures

France continues to dominate the global fragrance export market, producing far more than it consumes domestically. In 2024, French fragrance exports reached a staggering €8 billion, reflecting a 13.6% growth rate over the year and doubling in value over the past five years. This performance solidifies France’s role as the world’s leading exporter of luxury fragrances.

"The French perfumery sector recorded €8 billion in exports in 2024, with a growth rate of 13.6%, making it the most dynamic segment of the entire cosmetics industry." - FEBEA

The scale of production is equally impressive. France’s domestic glass industry manufactures 769 million bottles annually for use in perfumery and cosmetics. Over 90% of French perfume production is exported, a figure that highlights the global demand for French fragrances. The industry has also evolved to meet the needs of niche and limited-edition brands. While traditional suppliers often require minimum order quantities (MOQs) of 10,000–50,000 units, newer "short run" suppliers now offer MOQs as low as 1,000 units, making smaller-scale production more accessible.

This dominance in exports contrasts sharply with the consumption patterns seen within France and across Europe, revealing a fascinating divide between production and domestic demand.

French and European Consumption Patterns

Despite its unmatched production capabilities, France’s domestic fragrance consumption remains modest compared to its export figures. This contrast becomes even more apparent when examining consumption trends across key European markets.

Germany leads the European fragrance market, with a domestic market valued at €950 million - accounting for 30% of Europe’s total. German consumers show a strong inclination toward premium, sustainable, and organic fragrances. In France, the domestic market stands at €600 million, representing 19% of the European market. French consumers tend to favour artisanal, niche, and heritage brands, reflecting the country’s long-standing appreciation for craftsmanship and exclusivity. Meanwhile, the UK market is valued at €700 million (22% market share), driven largely by younger consumers who are drawn to personalised and niche fragrances.

Sustainability is also playing a transformative role in consumption habits. By 2025, 59% of French consumers reported purchasing perfume refills, reflecting a growing commitment to eco-friendly practices. Additionally, major French fragrance producers have reduced the weight of glass bottles by 15–20%, with plans to cut another 20% by 2030. These shifts demonstrate how France is blending its heritage of fine craftsmanship with a forward-thinking approach to environmental responsibility.

Leading French Perfume Brands in 2026

Chanel, Dior, and Guerlain Market Performance

France’s rich perfume heritage continues to thrive, with iconic brands like Chanel S.A., Parfums Christian Dior, and Guerlain leading the charge. The French fragrance market is projected to grow from €5.4 billion in 2025 to €9.1 billion by 2032, with an annual growth rate of 7.8%. In 2026, Chanel and Dior maintain their global dominance, while Guerlain remains a significant player in shaping industry trends.

These renowned houses balance their storied traditions with forward-thinking strategies. AI-driven personalisation and biotech-derived aroma chemicals, such as sustainable alternatives to sandalwood and musk, are reshaping product development. These innovations cater to the rising demand for clean-label and allergen-compliant ingredients. Additionally, mood-focused fragrances featuring notes like lavender and bergamot have become a staple in new releases, reflecting evolving consumer preferences. Scento’s customer data further highlights how these strategies resonate with buyers.

Top 10 Brands: Scento Customer Data

Scento’s analysis of 711 French customers offers valuable insights into shifting consumer behaviour. Both established luxury brands and niche artisanal labels are thriving, as buyers increasingly seek variety and personalisation in their fragrance choices. Many consumers now opt for smaller decant sizes - 2ml, 5ml, or 8ml - before committing to full-size bottles that often exceed €300. This "try-before-you-buy" approach not only reduces financial risk but also allows for the exploration of diverse scents, aligning perfectly with the trend of building personalised fragrance wardrobes. These insights underscore France’s continued leadership in the luxury fragrance market.

Your Personal Fragrance Expert Awaits

Take our quick scent quiz to discover authentic designer and niche fragrances matched to your taste — explore them as 2–8ml decants and samples, so you can try each one before committing to a full bottle.

Find Your ScentFrench Consumer Purchasing Patterns

Scento’s latest analysis highlights how French consumers are reshaping fragrance market trends, moving away from traditional full-bottle purchases toward more flexible and exploratory habits. Based on data from 711 French customers, there’s a clear preference for smaller formats like 2 ml, 5 ml, and 8 ml decants. This shift reflects a growing interest in personalised fragrance experimentation, supported by decant trials, subscription models, and a rising demand for niche perfumes.

Decant Purchases vs. Full Bottles

French consumers are embracing a "try-before-you-buy" mindset, using decants to sample fragrances before investing in full bottles. This approach aligns with the idea of a fragrance wardrobe, particularly popular among Gen Z and Millennials, who prefer curating scents for specific occasions, moods, or seasons rather than sticking to a single signature fragrance. Moreover, sustainability plays a significant role in full-bottle purchases, with 59% of French buyers opting for refills as of 2025. This evolving purchasing behaviour opens the door for subscription models that redefine how fragrances are owned and experienced.

Monthly Subscription Adoption Rates

Scento’s 8 ml monthly subscription service, priced at €12,90, has gained traction among French consumers seeking variety without the commitment of bulk purchases. The 8 ml size is especially appealing for travel, meeting carry-on liquid restrictions. This subscription model complements the fragrance wardrobe concept by letting customers rotate scents seasonally while maintaining a manageable collection. Alongside subscriptions, the balance between niche and designer fragrances sheds light on shifting consumer preferences.

Niche vs. Designer Purchase Split

The demand for niche fragrances is growing rapidly in France, with an annual growth rate of 13%. Scento’s data reveals that French consumers increasingly favour artisanal brands over traditional luxury houses. This preference reflects a desire for originality and craftsmanship, echoing France’s rich perfume heritage. While designer fragrances remain a staple, the availability of decant formats has made it easier to explore lesser-known brands. This balance highlights the sophistication of French buyers, who value both the legacy of established houses and the innovation of niche creators.

Niche Perfume Market Growth

The niche perfume market is thriving, with an annual growth rate of 13%, far outpacing the broader fragrance market’s 7.8% growth. This surge reflects a growing consumer appetite for distinctive and personalised scent experiences. In fact, 33.6% of buyers now lean towards unique fragrance combinations rather than mainstream options. Artisan brands are standing out by focusing on creating a strong olfactory identity and ensuring transparency in their ingredient sourcing.

Sustainability has become a key driver in this expansion. Niche perfume houses are leading the charge by adopting bio-based, upcycled, and natural ingredients, aligning with evolving European allergen regulations. Many are also embracing refillable packaging systems to comply with the EU Packaging and Packaging Waste Regulations. These efforts not only meet regulatory requirements but also allow brands to command a premium of 15–25% for their environmentally conscious formulations.

The digital world has played a major role in this growth. Social media fragrance communities have made it easier for consumers to discover lesser-known labels through reviews and decant sampling. This digital shift complements artisan brands’ storytelling strategies, enabling them to connect with audiences in more meaningful ways. Many brands are now testing the waters with smaller production runs, limited editions, and pilot launches to gauge market interest. This approach is helping artisan brands carve out a stronger presence in the fragrance industry.

Artisan Brand Performance

The success of niche perfumes is evident in the performance of key brands. Independent names like Byredo, Le Labo, and Diptyque have outpaced market growth by focusing on scents that tell stories tied to specific locations or cultural themes. Similarly, French artisan brands such as Serge Lutens and Frédéric Malle have embraced limited-production models, appealing to consumers who value exclusivity and craftsmanship.

These developments tie back to France’s strong export performance, with niche and artisanal lines now accounting for 20% of global perfume sales. Small-batch producers have successfully bridged the gap between niche appeal and mainstream recognition, further solidifying their position in the market.

Scento’s Niche Fragrance Catalogue

Scento has tapped into this growing demand with a catalogue featuring over 1,000 niche fragrances, catering specifically to French consumers’ interest in artisan scents. The platform offers flexible decant sizes - 2 ml, 5 ml, and 8 ml - making it easier for customers to explore lesser-known brands before committing to full-sized bottles. Among Scento’s 711 French users, trial sizes have proven especially popular for discovering new artisan houses.

The 8 ml monthly subscription, priced at €12,90, aligns with the trend of rotating seasonal scents. This model supports the "fragrance wardrobe" concept embraced by Millennials and Gen Z, while also addressing practical needs like travel-friendly formats. Shipping data further reveals that French customers are particularly drawn to brands with a focus on ingredient transparency and sustainable practices. By curating decant sizes that encourage exploration, Scento meets the growing demand for artisanal, thoughtfully crafted fragrances.

Market Projections Through 2030

Revenue and Growth Forecasts

The French perfume market is projected to grow from €3.23 billion in 2025 to €5.15 billion by 2034, with an annual growth rate of 5.36%. This trajectory not only highlights steady expansion but also reflects the interplay between traditional craftsmanship and modern consumer demands. While France continues to lead in heritage expertise, Germany is expected to dominate the European market share by 2034, and Russia is poised to become the fastest-growing market in the region. In 2025, the Eau de Parfum segment accounted for €1.31 billion, making it the largest contributor, while the Eau Fraiche category is on track to grow the fastest. Meanwhile, online distribution channels, which generated €1.82 billion in 2025, are reshaping how consumers shop for fragrances. These trends also emphasize the growing importance of sustainable practices shaping production and distribution.

Sustainability Practices and Sourcing

Sustainability is no longer a niche trend but a driving force in the fragrance industry. Ethical sourcing and eco-friendly packaging are becoming non-negotiable as brands align with evolving European allergen regulations and stricter packaging standards. Globally, the perfume market is expected to hit €69.25 billion by 2030, with sustainable practices playing a crucial role in this growth. For instance, in April 2021, LVMH and Sephora introduced MAISON 21G, an AI-powered tool for personalized fragrance recommendations. This reflects a broader industry shift toward transparency and ethical production, meeting the expectations of increasingly conscious consumers.

Scento’s Product Expansion Plans

Scento is expanding its product range with new 30 ml+ bottle sizes, bridging the gap between discovery and full-size collections. This addition complements smaller decant options (2 ml, 5 ml, and 8 ml) and caters to the rising demand for travel-friendly formats that combine convenience with durability. The 30 ml bottle offers around 300–450 sprays, providing an ideal step-up for customers transitioning from sampling to larger investments. This initiative underscores the adaptability and forward-thinking approach that solidify France’s role in the evolving global fragrance market.

Conclusion

By 2026, France remains firmly established as the world’s perfume capital, a title it has upheld through centuries of expertise and a thriving industry generating over €10 billion in revenue. In 2024 alone, exports hit €8 billion, marking a 13.6% year-over-year increase, underscoring the sector’s impressive profitability. With a 4.16% share of the global market, France continues to lead the way in perfumery.

Consumer preferences have shifted significantly, focusing more on personal expression and environmentally conscious choices. Niche perfumery now represents 10% to 12% of the French market and is expanding at an annual rate of 13%. Younger generations, particularly millennials and Gen Z, are driving this change, accounting for over 58% of indie fragrance purchases in 2025. Meanwhile, online sales have grown by 34%, now making up 19% of the market. These trends highlight a move away from mass-market offerings toward artisanal creations and transparent ingredient narratives.

Scento is at the forefront of this transformation, offering European shoppers access to over 1,000 designer and niche fragrances through decants in sizes of 2 ml, 5 ml, and 8 ml, with subscriptions starting at €12.90 per perfume. The introduction of 30 ml+ bottles will provide a bridge between sampling and full-size collections, aligning with France’s projected market growth from €3.23 billion in 2025 to €5.15 billion by 2034.

As sustainability and clean beauty standards reshape the industry, France’s rich heritage and expertise position it to lead this new era. The fusion of traditional craftsmanship with modern advancements is setting the stage for both established brands and emerging artisans, giving European consumers unparalleled access to genuine French perfumery through flexible, discovery-focused options.

FAQs

Why are French perfume exports so much higher than France’s domestic sales?

France’s reputation as a global hub for perfumery and cosmetics is well-earned, with its perfume exports outpacing domestic sales. In 2024, the country exported perfumes worth an impressive €22.5 billion, underscoring its position as a major supplier to international markets. This highlights the export-oriented nature of the French perfume industry, where domestic sales play a comparatively smaller role.

How do I choose between a decant, a 30 ml bottle, and a full-size perfume?

When deciding, consider your personal needs and preferences:

- Decant: Perfect for trying out a new fragrance or for travel, thanks to its compact size and TSA-friendly design.

- 30 ml bottle: A convenient middle ground, suitable for regular use and moderate travel.

- Full-size bottle: Ideal for long-term use at home or if you’re devoted to a particular scent.

Your choice should align with how often you’ll use it, how portable you need it to be, and how committed you are to the fragrance.

What makes a perfume “niche” in France, and why is it growing so fast?

In France, a perfume earns the label "niche" when it comes from specialised fragrance houses that focus on creativity, exclusivity, and craftsmanship rather than catering to the mass market. These scents are often produced in limited quantities, using rare or natural ingredients, and tell distinctive olfactory stories.

The surge in niche perfumes can be linked to a growing desire for personal expression, the appeal of high-quality materials, and the allure of artisanal techniques. Additionally, the rise of e-commerce and social media has amplified their visibility, making these unique fragrances more accessible to a global audience.