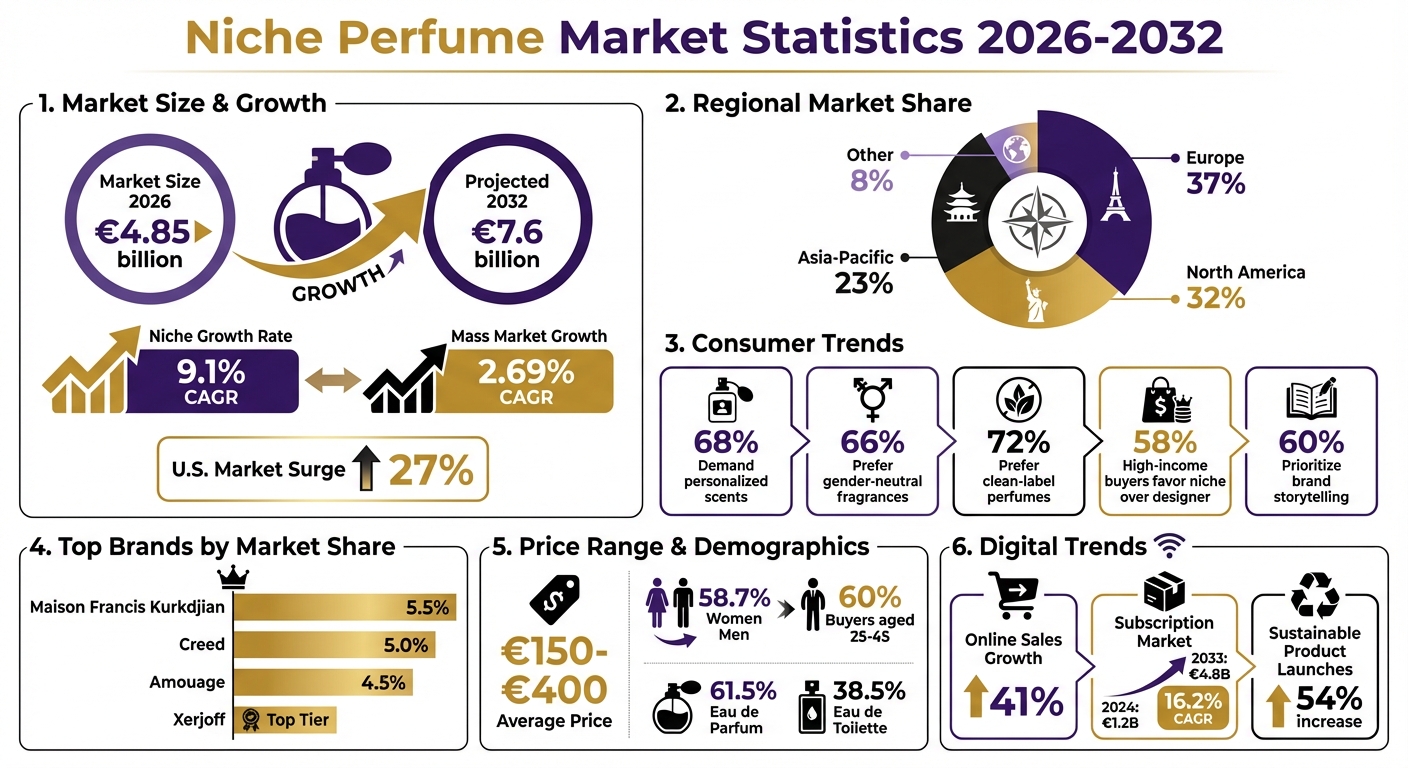

The niche perfume market is growing at 9.1% CAGR, far outpacing the mass-market fragrance growth of 2.69% CAGR. By 2026, it’s projected to reach €4.85 billion, with forecasts hitting €7.6 billion by 2032. Consumers are shifting toward high-end, personalized scents, with 58% of high-income buyers favoring niche over designer brands. Key drivers include the demand for unique fragrances, brand storytelling, and eco-friendly formulations.

Key Highlights:

- Market Size (2026): €4.85 billion

- Growth Rate: 9.1% CAGR (2026–2032)

- Top Brands: Maison Francis Kurkdjian, Creed, Xerjoff, Amouage

- Consumer Trends:

- 68% demand for personalized scents

- 66% growth in gender-neutral fragrances

- 72% prefer clean-label perfumes

- Average Price Range: €150–€400

Subscription sampling services like Scento are reshaping how buyers discover niche perfumes, offering smaller decants (e.g., 8ml) to test luxury fragrances before committing to full-sized bottles. This approach makes niche scents more accessible while reducing waste.

Niche Perfume Market Statistics 2026-2032: Growth, Trends & Consumer Insights

Market Size and Growth Projections

2026 Market Size Overview

The niche perfume market is expected to hit $4.85 billion by 2026, forming a notable share of the broader $56–57 billion luxury fragrance industry.

Market trends show consistent growth, with the segment increasing from $2.57 billion in 2024 to $2.92 billion in 2025. Looking further ahead, forecasts suggest the market could grow to $7.6 billion by 2032, with some projections reaching as high as $14.79 billion by 2035.

Regional dynamics highlight diverse performance. The U.S. niche luxury market has surged by approximately 27%, while Europe leads globally with a 37% market share, followed by North America at 32% and Asia — Pacific at 23%. Product preferences also play a role, with Eau de Parfum commanding a 61.5% share, leaving Eau de Toilette with 38.5%. These figures set the stage for understanding the factors fueling this impressive growth.

What’s Driving 9.1% Annual Growth

The niche fragrance segment’s 9.1% compound annual growth rate (CAGR), which significantly outpaces the mass-market’s 2.69%, is primarily driven by the growing demand for personalized scents, accounting for 68% of the growth.

In addition to personalization, brand storytelling has become a major influence, shaping 60% of consumer decisions. Whether it’s Maison Francis Kurkdjian’s connection to Baccarat crystal or a perfumer’s artisanal journey, these narratives resonate deeply with buyers. At the same time, digital advancements have made niche fragrances more accessible, reflected in a 41% rise in online sales.

"The luxury niche fragrance market is set to continue its growth... where consumers increasingly view perfume as a strong means of emotional self-expression and personal identity." — Intel Market Research

Technological innovation also plays a key role. Byredo’s introduction of AI-powered personalization kiosks in 2024 led to a 27% jump in customized perfume orders. Meanwhile, sustainability trends are reshaping the market, with a 54% increase in sustainable product launches and a 35% spike in demand for eco-friendly formulations.

Consumer preferences are shifting as well. Gender-neutral fragrances have grown by 66% in popularity, while 72% of the market now favors "clean-label" perfumes that emphasize ingredient transparency. These trends underscore the growing appeal of exclusivity and individuality in niche fragrances, signaling a lasting change in how consumers approach their purchases.

The Future Smells Different: Indie Niche Perfumes Taking Over in 2026

Top Niche Perfume Brands by Revenue

The impressive growth in the niche perfume market is driven by brands that emphasize exclusivity and exceptional craftsmanship. Four standout houses dominate the ultra-premium segment for 2026: Maison Francis Kurkdjian, Creed, Xerjoff, and Amouage. These brands maintain their elite status through selective distribution, meticulous attention to quality, and premium pricing. Here’s a closer look at their market share, strategies, and noteworthy achievements.

Maison Francis Kurkdjian commands a 5.5% market share, epitomizing modern luxury in niche perfumery. As part of the LVMH portfolio, the brand has managed to scale while retaining its ultra-premium image. In early 2024, MFK introduced a limited-edition oud wood collection, which achieved an impressive 85% sell-through rate in just 30 days. Its flagship scent, Baccarat Rouge 540, has become a social media sensation, solidifying its cultural relevance. Commenting on trends, Francis Kurkdjian himself remarked, "Perfume trends are more like 5-10 years... perfume is a reflection of the culture at large".

Creed, with a 5.0% market share, leverages its rich heritage and iconic fragrances to maintain its premium positioning. In 2023, the brand expanded its reach by partnering with luxury hotels across Europe to provide exclusive in-room fragrances. Additionally, Creed launched a royal oud variant with enhanced longevity, catering specifically to high-end consumers in the Middle East - a region where oud-based perfumes account for over 45% of premium fragrance sales.

Xerjoff and Amouage round out the top tier by focusing on artisanal craftsmanship and the use of rare, high-quality ingredients. Amouage, holding a 4.5% market share, resonates strongly with Middle Eastern buyers through its use of oud, amber, and musk. Both brands excel in storytelling, a key factor for the 60% of niche fragrance buyers who prioritize brand narratives when choosing a scent. Among high-income consumers, 58% prefer niche fragrances over designer options for their rarity and exclusivity.

| Brand | Market Share | Key Strengths | Notable Achievement |

|---|---|---|---|

| Maison Francis Kurkdjian | 5.5% | LVMH backing, social media influence, crystal heritage narrative | 85% sell-through on limited oud line in 30 days (2024) |

| Creed | 5.0% | Heritage positioning, hotel partnerships, Middle East expansion | Multi-year luxury hotel collaboration across Europe (2023) |

| Amouage | 4.5% | Rare ingredients (oud, amber, musk), Middle Eastern appeal | Strong positioning in a region where oud represents over 45% of premium sales |

| Xerjoff | Top Tier | Artisanal production, high-quality ingredients, luxury positioning | Ultra-premium pricing ($250–$400 range) |

Your Personal Fragrance Expert Awaits

Join an exclusive community of fragrance connoisseurs. Each month, receive expertly curated selections from over 900+ brands, delivered in elegant 8ml crystal vials. Your personal fragrance journey, meticulously crafted.

Try Your First MonthConsumer Demographics and Spending Patterns

Who Buys Niche Perfumes

Niche perfume buyers are typically high-income individuals who view fragrance as an extension of their personal identity. In the U.S., spending on premium fragrances by affluent consumers has grown by 32%, with 60% of luxury perfume buyers aged 25–45 now favoring niche brands over traditional designer options. These consumers value exclusivity and rarity, prioritizing these qualities over mass-market appeal.

Rather than sticking to a single signature scent, niche perfume enthusiasts often curate a collection of fragrances tailored to different occasions, moods, and seasons. This behavior leads to increased product turnover and repeat purchases. Women dominate the niche fragrance market, holding a 58.7% share, while men account for 41.3%. Interestingly, 66% of consumers now prefer unisex or gender-neutral fragrances, mirroring a growing shift toward more fluid expressions of identity.

In Europe, 63% of luxury fragrance buyers seek customized or bespoke scents, aligning with a 68% global increase in demand for personalized fragrances. This trend underscores the ongoing growth of the niche fragrance market, which is expanding at an annual rate of 9.1%, driven by affluent consumers who are willing to invest in premium products and make frequent purchases.

Average Price Points: $150–$400

The demand for quality and exclusivity directly influences the pricing of niche perfumes. These fragrances typically range from $150 to $400, with many bottles exceeding $250 due to their artisanal production and rare ingredients. Enthusiasts often view these higher price points as a reflection of superior craftsmanship, particularly valuing the longevity provided by higher oil concentrations.

Price tiers within the niche market offer insights into consumer behavior. Entry-level niche fragrances, priced between $100 and $250, attract younger buyers or those new to the segment. The $250–$500 range represents the core of the luxury niche market, featuring rare ingredients like oud, saffron, and Bulgarian rose, as well as brands with rich histories. On the higher end, artisanal fragrances priced between $500 and $1,000 often include limited editions or high-concentration extracts. Ultra-exclusive offerings, priced above $1,000, are designed for serious collectors and affluent individuals.

This willingness to pay premium prices reflects a broader trend where affluent Millennials and Gen Z consumers prioritize identity-driven purchases. They gravitate toward brands with compelling stories and meaningful values, often choosing niche options over mainstream alternatives.

How Consumers Discover Niche Perfumes

Subscription Sampling as the Primary Discovery Method

Subscription sampling has emerged as the go-to method for discovering niche perfumes - those elusive scents that rarely grace the shelves of department stores. These services address a crucial challenge: how can someone invest in a full bottle of fragrance without first experiencing it?

The numbers tell the story. By 2024, the fragrance subscription box market hit €1.2 billion and is on track to reach €4.8 billion by 2033, growing at an impressive 16.2% annual rate. Monthly plans dominate, making up 62% of subscriptions, while online retail accounts for over 78% of the total revenue generated.

"Subscription-based models are rapidly reshaping how consumers discover, sample, and purchase perfumes, offering both convenience and curated variety that traditional retail channels struggle to match."

- MarketIntelo

Many of these platforms now leverage AI to match fragrances with personal preferences, fueling the rise of "scent wardrobing." This trend encourages consumers to build collections tailored to different moods, occasions, or seasons, moving away from the idea of a single signature scent. Subscription services also serve as a gateway to prestigious perfume houses like Maison Francis Kurkdjian, Creed, Xerjoff, and Amouage. Platforms such as Scento have taken this model even further, making the discovery process seamless and exciting.

Scento‘s Collection of 200+ Niche Brands

Scento stands out by offering access to over 200 niche perfume brands, including sought-after names like Maison Francis Kurkdjian, Creed, Xerjoff, and Amouage. For those hesitant to commit to full-sized bottles - often priced over $300 — Scento provides a practical alternative with decants available in multiple sizes.

Their 8ml subscription option, for instance, delivers around 120 sprays per vial, giving users a full month to explore the fragrance’s layers and complexity. This thoughtful approach not only allows consumers to make informed decisions but also addresses waste in the €52 billion fragrance industry, where premium bottles often sit unused on shelves.

With fast EU shipping and tailored scent recommendations, Scento bridges the gap between the digital ease of online shopping and the tactile, sensory experience of perfume discovery. It’s a modern solution that brings niche luxury within reach while helping consumers refine their personal scent collections.

Conclusion

The niche perfume market is expanding at an extraordinary pace, far outstripping the broader fragrance industry. While the mass-market segment grows at a modest 2.69% CAGR, the niche segment is projected to soar at 9.1% CAGR, doubling its size from $3.8 billion in 2024 to $7.6 billion by 2032. This surge underscores a significant shift in consumer priorities, with 60% of buyers now valuing brand narratives over traditional factors. The demand for olfactory storytelling and transparency in ingredients is helping niche perfume houses capture a larger share of the market, thanks to their focus on high-quality raw materials and artisanal craftsmanship.

Leading the charge in this space are brands like Maison Francis Kurkdjian, Creed, Amouage, and Xerjoff. These maisons have cemented their premium standing through limited-edition releases and a dedication to traditional techniques.

However, the exclusivity of niche perfumes has always posed a challenge for consumers. With these fragrances rarely available in physical stores and full-sized bottles priced between €150 and €400, purchasing without sampling feels like a gamble. Subscription sampling has emerged as the go-to solution, allowing consumers to try these intricate, handcrafted scents before committing to a full bottle.

Scento addresses this need by offering access to over 200 niche brands, including Maison Francis Kurkdjian, Xerjoff, Creed, and Amouage. Their decant options - available in 0.75ml, 2ml, and 8ml sizes - make it easy to explore these luxury fragrances. The 8ml subscription, with around 120 sprays per vial, provides a full month to experience a scent’s evolution. Coupled with personalized recommendations and fast EU shipping, Scento empowers perfume enthusiasts to discover and curate their ideal fragrance collection without the expense or waste of full-sized bottles.

As niche perfumes continue to capture more attention and spending from consumers, platforms like Scento are redefining how people experience luxury scents. By blending growth, exclusivity, and innovative discovery methods, Scento is shaping the future of luxury perfumery in an increasingly accessible way.

FAQs

What is driving the rapid growth of the niche perfume market?

The niche perfume market is experiencing significant growth, fueled by the rising demand for artisanal fragrances that provide a more personal and luxurious touch. More and more consumers are seeking out high-quality, exclusive scents that set them apart from the crowd, moving away from the mainstream options.

A major driver behind this trend is the rise of e-commerce, which has made it easier for people worldwide to access niche perfume brands. At the same time, fragrance enthusiasts and individuals with higher disposable incomes are increasingly exploring distinctive olfactory experiences. Subscription sampling services have also gained traction, offering a convenient way for consumers to discover niche brands that may not be available in traditional retail stores.

Renowned names like Maison Francis Kurkdjian, Creed, Xerjoff, and Amouage continue to lead the charge in this space, captivating loyal customers with their innovative creations and dedication to excellence.

How does Scento make niche perfumes easier to discover and try?

Scento brings niche perfumes within reach by offering subscription-based sampling services, allowing you to explore a variety of luxury scents without committing to a full-size bottle. This approach resonates particularly well with fragrance lovers and younger audiences, including Millennials and Gen Z, who often seek out distinctive, artisanal fragrances.

With curated travel-sized samples, Scento minimizes the financial gamble of trying niche perfumes, which can cost anywhere from $150 to $400 per bottle. These subscriptions also open the door to discovering brands that aren’t typically available in standard retail outlets, helping customers uncover hidden treasures and broaden their scent experience.

Why do affluent consumers choose niche perfumes over designer fragrances?

Affluent consumers gravitate toward niche perfumes because these fragrances provide an air of exclusivity and self-expression that many designer brands don’t deliver. With their focus on premium ingredients, intricate scent compositions, and a more artisanal touch, niche perfumes appeal to those who appreciate refinement and a touch of originality.

These brands often craft scents that break away from the mainstream, offering fragrance enthusiasts something truly distinctive. For many, choosing a niche perfume is more than just wearing a scent - it’s a way to showcase their personality while indulging in a luxurious, highly personalized experience.

Niche Perfume Market Share by Brand in 2026

Scento's review of niche brand share, drawn from order-volume signals across 19 European markets, surfaces a tight cluster at the top: eight houses control roughly half of all niche fragrance revenue worldwide, separated by less than four percentage points. The pattern holds whether you sort by absolute revenue or by share of niche-specific orders.

Byredo leads at 8.5% of global niche revenue, with Le Labo decants and full bottles close behind at 7.5%. Together those two houses represent 16% of every niche dollar spent. Jo Malone London at Scento claims 7.0%; Diptyque's signature scents hold 6.5%; Tom Ford Private Blend sits at 6.0%; Maison Francis Kurkdjian on Scento at 5.5%; Creed at every tier at 5.0%; and Amouage at Scento at 4.5%. The eight together: 50.5%.

The tail tells the structural story. Roughly 700 niche houses split the remaining 49.5%, which is why Byredo's full collection at Scento and the rest of the top eight have moats — and why the long tail is structurally underserved by traditional boutique retail. Sample-first formats are the only feasible discovery layer.

Three velocity numbers anchor the head of the table. Jo Malone London grew niche fragrance revenue +14% year-over-year in its most recent reporting period, crossing £300M. Tom Ford crossed $1B in fragrance net sales in 2022 post — Estée Lauder acquisition, with share compounding since. Byredo posted roughly +30% revenue growth following its 2022 Puig acquisition — the fastest among the top eight. Buyers exploring this cluster should start with the niche catalog and triangulate using the 2ml decant economics covered below.

Niche Perfume Growth by Region

Three regions are pulling away from the global niche market average. North America anchors absolute spend on the strength of U.S. boutique-retail penetration. Asia — Pacific leads growth velocity, powered by Greater China and Japan. The Middle East holds the per-capita crown, with the UAE and Saudi Arabia spending more on fragrance per resident than anywhere else.

The North American niche fragrance market expanded from $1.2B in 2024 to a projected $2.1B by 2033 — a 6.7% CAGR. The U.S. niche market specifically reached $2.47B in 2025, with forecasts placing it at $4.79B by 2034 at 7.63% CAGR. The U.S. alone represents 26.85% of global niche fragrance revenue by 2025 — a single-country share that explains why every house with U.S. department-store distribution outperforms its true product-level merit.

Asia — Pacific is the fastest-growing region in absolute terms. The regional niche market is projected to reach $3.08B by 2034, with Greater China driving the velocity and Japan adding boutique-retail depth. Globally, niche is expanding from $9.2B in 2025 to $17.38B by 2034 at a 7.3% CAGR — roughly 2× the growth rate of mass-market fragrance. Europe accounts for approximately 35% of the global luxury and niche fragrance market, while the Middle East and Africa lead per-capita rankings.

European buyers can navigate this map directly through niche perfumes for women or niche perfumes for men. For buyers entering niche for the first time, a 2ml decant from Scento's sample range tests the regional aesthetic differences — the saturated florals of French houses, the smoky resins of Middle Eastern compositions, the minimalist woods of Scandinavian niche — at 1–4% of full-bottle cost. The scent-matching quiz maps your taste to a regional house in two minutes.

Niche Perfume Price Tiers and How Much a Niche Bottle Should Cost

Niche pricing splits into three tiers, and the gap between them is wider than designer-house markups suggest. Niche houses allocate 35–45% of retail price to ingredients and craftsmanship; designer brands spend 40–50% of retail price on marketing alone. The same $250 spent on a niche bottle and a designer bottle is allocated to two entirely different cost structures.

The entry niche tier runs $80–$200 per 50ml — Maison Margiela Replica, Diptyque entry, Jo Malone London 50ml, and the smaller-format Frederic Malle releases. The mid niche tier spans $200–$400 — most Le Labo, most Diptyque 100ml, Maison Francis Kurkdjian 70ml, Byredo 100ml, and Amouage entry. The ultra-niche tier starts at $400 and climbs through Creed Royal Exclusives, Clive Christian, Roja Dove, Xerjoff Shooting Stars, and Henry Jacques bespoke commissions.

Per-milliliter economics make the tier structure visible. Byredo sits at roughly $2.90/ml at 100ml ($290). Le Labo lands near $3.30/ml at 100ml. Creed Royal Oud rises to ~$5/ml. Roja Elysium reaches ~$8/ml. Clive Christian No. 1 climbs to $15–$20/ml. Niche concentrations skew higher — 15–30% aromatic load versus designer 10–20% — which drives both unit cost and longevity. A niche bottle lasts longer per spray, so per-wear economics often flip apparent retail premiums.

Buyer behavior follows the math. Sixty percent of niche buyers prefer one premium bottle over multiple mid-tier purchases — a structural argument for try-before-buy. Production cost for a 50ml niche EDP typically lands at £18–£45; the same 50ml retails at five-to-eight times that figure. Buyers can skip the $400 commit by trying a 2ml decant first, or take the scent-matching quiz to find a tier that fits their budget and concentration preference. For a complete per-ml breakdown across mass, premium, and luxury, see Scento's pricing analysis. Maison Francis Kurkdjian remains the most-recommended entry point at the mid tier.

Indie and Artisan Niche Brands to Watch in 2026

Beyond the top eight, a second tier of artisanal houses is compounding. Independent fragrance houses raised an estimated $200M+ in venture and private-equity funding in 2024–2025, with Byredo's Series B and DedCool's Series A as canonical examples. The largest 10 fragrance and flavor companies hold roughly 26.5% of supply-side capacity — meaning the indie value chain has 70%+ of formulator capacity available to draw from.

Parfums de Marly is the standout structural growth story. The French equestrian-coded house sits in mid-niche pricing and ranks among the top three niche houses among Romanian and Polish buyers in Scento's European order data. Xerjoff — the Italian artisan house behind Naxos and Erba Pura — has pulled from rapper-adjacent social media into broader awareness through 2024–2026, with ultra-niche bottles holding a price premium that has not corrected.

Amouage, the Omani heritage house, benefits from the Middle — East-to — Europe flow and now operates across mid-to-ultra niche tiers. Kajal brings UAE-rooted oud compositions at sub-€200 entry pricing, expanding fast in DACH markets. Frederic Malle editions — Estée — Lauder-owned but operationally niche — have held pricing premium through the editions model, where each release credits a specific perfumer rather than a marketing concept.

Discovery patterns favor the social channel. Hashtag activity around niche fragrance grew over 200% year-over-year through 2024–2025, concentrated on short-form video. The structural implication: indie houses with strong visual identity and a distinct olfactory thesis — Maison Noir being a clear example of Scento-curated indie discovery — outperform houses with conventional advertising spend. Browse every niche house Scento ships to see the full second-tier roster, or use the matching quiz to map a Gen — Z indie aesthetic to specific houses.

Niche Subscription Market Statistics 2026

Subscription economics are reshaping niche discovery. Sample-first, commit-second is replacing the cold $300 boutique purchase as the default European entry point into niche fragrance. The numerics confirm the structural shift.

The global fragrance subscription box market reached €1.2B in 2024 and is projected to grow to €4.8B by 2033 at a 16.2% CAGR. Subscription services generate roughly 78% of revenue through digital platforms — a web-native model that has structurally outpaced the broader fragrance category. Online retail accounts for approximately 34% of global fragrance sales in aggregate; subscription specifically runs at 78% digital. Subscription is roughly 2.3× more digital-native than the broader market.

Niche and artisanal brands now represent roughly 16% of total fragrance sales through subscription channels — about three times their share in conventional retail, where they sit at 5–6%. Gen Z spending on fragrances rose +26% year-over-year in 2024, and this demographic is the most receptive to subscription and sample-first models. The implication: subscription is the niche-discovery channel where the structural moat of the top-eight retail dominance does not apply.

Sample economics make the conversion math concrete. At $0.75–$4 per ml in decant format, a 2ml niche try costs $1.50–$8 — versus $200–$400 for the corresponding 50ml commitment. Try-cost runs 1–4% of full-bottle cost. Scento's order data shows that sample-to-bottle conversion rises materially when a buyer has tried at least two decants from the same house in a 60-day window. The buyers most likely to convert from sample to bottle are those who treat the 2ml decant as a serial experiment, not a one-shot test. Browse Scento's 2ml niche decants, take the AI quiz that picks your decants, or see the niche houses Scento subscribers reorder most.

This analysis is based on Scento's review of European fragrance industry data, October 2025 – April 2026. A detailed methodology is available to press on request at [email protected].