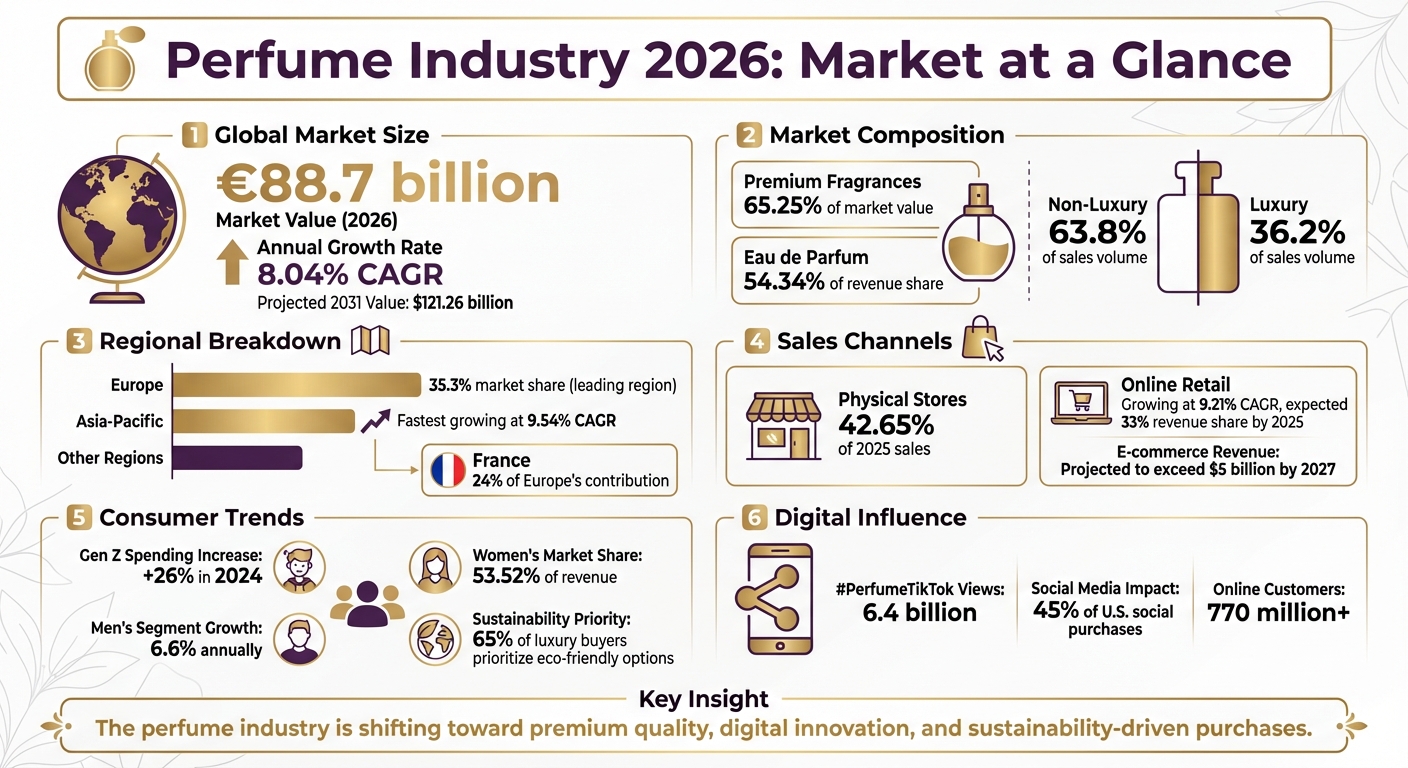

The perfume industry in 2026 is thriving, with global sales projected to reach €88.7 billion, driven by 8.04% annual growth. Key drivers include increased spending by Gen Z, a shift to premium and niche fragrances, and the rise of online retail, growing at 9.21% CAGR. Here’s a quick snapshot:

- Premium dominates: 65.25% of market value in 2025.

- Gen Z impact: Fragrance spending up 26% in 2024.

- Online growth: E-commerce expected to claim 33% of revenue by 2025.

- Regional trends: Europe leads with 35.3% market share, while Asia — Pacific grows fastest at 9.54% CAGR.

- Sustainability matters: 65% of luxury buyers prioritize eco-friendly options.

This evolution reflects changing consumer habits, with a focus on personalization, digital innovation, and higher-quality formulations like Eau de Parfum. The industry is moving beyond mass-market appeal to cater to diverse, value-conscious, and digitally engaged buyers.

Perfume Industry 2026: Key Statistics and Market Trends

1. Scento Proprietary Statistics

Scento Proprietary Data: Insights into Modern Fragrance Discovery

Scento’s data offers a clear look at how consumers are approaching fragrance discovery in 2026, highlighting a shift in behavior and preferences.

Over 85,000 members are part of Scento’s fragrance community (Scento internal data). This growing group reflects a movement away from traditional retail shopping, as more people seek curated and personalized fragrance experiences.

The Scento catalog includes more than 1,000 designer and niche perfumes (Scento internal data). From luxury brands to independent perfumers and rising niche labels, the collection represents the industry’s growing emphasis on variety and individuality.

75,000+ scent profile quizzes have been completed by Scento users (Scento internal data). This high number underscores a key trend: shoppers are looking for personalized guidance to navigate the overwhelming number of fragrance choices. The popularity of these quizzes demonstrates the value consumers place on tailored, data-driven recommendations over random purchases.

Another important insight: 8ml vials, offering about 120 sprays, allow users to explore fragrances without committing to full-size bottles (Scento internal data). These findings provide a glimpse into the evolving global fragrance market.

2. Global Market Size and Growth

The Perfume Market Continues Its Upward Trajectory

Global fragrance sales are on track to reach $88.7 billion by 2026, according to Global Market Insights. Other research firms estimate market sizes ranging from $60.26 billion to $82.38 billion for the same year, with projected growth rates of 8.04% CAGR (Mordor Intelligence; Research Nester).

The market’s growth trajectory varies slightly across reports, with CAGR projections between 5.4% (Global Market Insights) and 8.8% (SkyQuest) over the next decade. This growth is largely fueled by increasing disposable incomes and a rising preference for premium fragrances, as global income levels climb by 3.5% annually (Global Market Insights).

Premium fragrances dominated the market, making up 65.25% of total market value in 2025 (Mordor Intelligence). Meanwhile, Gen Z has become a key driver of growth, boosting their fragrance spending by 26% in 2024 (Mordor Intelligence). Eau de Parfum also stood out as a favorite, accounting for 54.34% of revenue share in 2025 (Mordor Intelligence).

In the next section, we’ll dive into regional trends to uncover where this growth is happening most dynamically.

3. Regional Market Breakdown

Europe Leads, Asia — Pacific Races Ahead

Europe continues to dominate the global perfume market, holding an impressive 35.3% of the global market share in 2024. France alone accounts for a striking 24% of Europe’s contribution (Perfume Market Report; SkyQuest). The region is also expected to drive 37% of the growth in the luxury segment by 2030, solidifying its position as a leader in high-end perfumery (Global Market Insights).

Meanwhile, Asia — Pacific is emerging as the fastest-growing region, with a projected compound annual growth rate (CAGR) ranging between 9.54% and 10.66% through 2031. This rapid growth is largely fueled by expanding middle classes in countries like China and India (Mordor Intelligence; Research Nester). The luxury perfume market in this region is also set to grow at a steady 7.9% annual rate through 2030 (Global Market Insights).

The Middle East represents a high-value market, deeply rooted in traditions of opulent and long-lasting fragrances such as oud and attars. Consumers in this region exhibit high per-capita spending, with luxury perfumes often priced at approximately $325 for a 100ml bottle (SkyQuest).

In North America, there’s a noticeable shift in consumer behavior. Buyers are moving away from sticking to a single signature scent and are instead building diverse fragrance wardrobes. For instance, women are 37% more likely than men to select perfumes based on their mood for the day (Research Nester).

Next, we’ll delve into how these regional preferences shape the industry’s key sales channels.

4. Sales Channels

Physical Stores Still Dominate, But Online Is Catching Up Fast

Physical stores remain a cornerstone of fragrance sales, contributing 42.65% to projected 2025 sales and generating $11.82 billion in 2024. With 60% of consumers preferring in-person testing, the appeal of experiencing scent, texture, and packaging firsthand is clear (Mordor Intelligence; Global Market Insights). This tactile connection continues to anchor traditional retail’s importance, even as the industry evolves.

Meanwhile, online retail is rapidly gaining traction, growing at an impressive 9.21% CAGR through 2031 and reaching over 770 million customers (Mordor Intelligence; Research Nester). To bridge the sensory gap, digital platforms are now leveraging AI-driven profiling and offering subscription-based trials, making it easier for consumers to explore fragrances without stepping into a store (Mordor Intelligence).

Social media has also emerged as a powerful driver of fragrance discovery. Platforms like TikTok play a significant role, influencing 45% of U.S. social purchases. The hashtag #PerfumeTikTok alone has amassed 6.4 billion views, while Gen Z increased their fragrance spending by 26% in 2024 (Research Nester; Mordor Intelligence).

The online fragrance market is expected to claim 33% of revenue share by 2025, with e-commerce revenue projected to surpass $5 billion by 2027 (Research Nester). Brands are blending the best of both worlds through omnichannel strategies, such as physical "Scent Stations" and vending machine concepts, combining the tactile joys of in-store shopping with the convenience of digital exploration (Mordor Intelligence).

These evolving sales channels highlight the dynamic shifts in consumer behavior and spending patterns.

5. Consumer Spending and Demographics

Women Lead Spending, But Men Are the Fastest — Growing Segment

The fragrance market continues to evolve, with consumer spending trends reflecting notable shifts in buying behavior.

Women remain the primary buyers, contributing 53.52% of market revenue in 2026, though this marks a decline from 61.7% in 2025. This dominance ties back to long-standing associations between fragrance, grooming, and personal identity.

Meanwhile, the men’s segment is expanding rapidly, with a 6.6% annual growth rate. Male teens, in particular, are driving this trend, showing a 26% year-over-year increase in spending. Social media platforms like TikTok and Instagram have played a pivotal role in reshaping how men view fragrance, integrating it into broader grooming routines.

On a global scale, the average consumer contributes $8.19 to fragrance revenue. Certain regions stand out, such as Saudi Arabia, where oud and oriental scents hold strong appeal, and the US, where fragrance sales are projected to reach €9 billion by 2026.

Younger buyers are leaning toward quality over quantity, with over 60% in developed markets preferring a single, high-quality fragrance. Additionally, sustainability matters - 65% of luxury consumers are willing to pay a premium for eco-friendly options.

In terms of pricing, medium-priced fragrances held 39.1% of the market in 2025. By 2026, non-luxury fragrances are expected to account for 63.8% of sales, while luxury options will make up 36.2%. These shifts highlight changing priorities and preferences in the global fragrance market.

Your Personal Fragrance Expert Awaits

Join an exclusive community of fragrance connoisseurs. Each month, receive expertly curated selections from over 900+ brands, delivered in elegant 8ml crystal vials. Your personal fragrance journey, meticulously crafted.

Try Your First Month6. Production and Sales Volume

Fragrance: From Occasional Luxury to Everyday Staple

Consumer habits have reshaped the fragrance market, transforming it into a daily essential rather than a rare indulgence.

The global fragrance market is projected to grow significantly, with estimates placing its value between $64.47 billion and $88.7 billion by 2026. This rise in revenue reflects a shift in production priorities. Mass-market fragrances are expected to lead this growth, driven by consumers seeking affordable yet high-quality options.

Producers are increasingly focusing on higher-concentration formats like Eau de Parfum and Parfum, which offer longer-lasting performance and greater value for money. This aligns with changing consumer expectations, as buyers prioritize fragrances that deliver both durability and a sense of worth.

France remains a powerhouse in global perfume production, exporting approximately $7 billion worth of perfume in 2022, with over 50.5% of its output going to international markets. The Grasse region, known for its expertise in ingredient development, continues to be a hub of innovation. By 2026, Europe is expected to command around 35% to 36% of the global perfume market share.

Another driver of production and sales growth is the rise of "fragrance wardrobing." This trend sees consumers curating collections of scents tailored to different moods, seasons, and occasions. As buyers move away from relying on a single signature fragrance, the industry is adapting to meet the demand for variety and personalization.

7. Top — Selling Brands and Companies

The Power Players Shaping the $60B+ Market

The fragrance market, valued at over $60 billion, is shaped by a few dominant players. Global giants like LVMH, L’Oréal, Coty, Estée Lauder, Chanel, and Puig lead the charge, commanding both the luxury and mass-market sectors. Their ability to balance exclusivity with accessibility has been key, as consumers increasingly seek high-quality fragrances at a range of price points.

Currently, non-luxury products make up 63.8% of total sales, while the premium segment generates 57.5% of the revenue. This balance highlights a market where luxury brands maintain their prestige, while mass-market offerings grow by delivering affordability without compromising quality. Recent product launches illustrate this evolving dynamic.

In August 2023, Coty introduced Burberry Goddess, achieving record-breaking sales and showcasing its dual-market strategy. Two years later, Miu Miu launched Miutine, a premium eau de parfum featuring wild strawberry and brown sugar, capitalizing on the gourmand trend. Chanel also strengthened its luxury position with BLEU DE CHANEL L’EXCLUSIF in August 2025, incorporating sustainably sourced sandalwood from New Caledonia. These launches underline a growing consumer appetite for fragrances that blend innovation with quality.

"Mass and prestige markets are merging, with premium brands in mass channels and value-driven luxury brands excelling." - Larissa Jensen, SVP and Global Beauty Advisor, Circana

Mass fragrances are currently the fastest-growing segment, with an expected growth rate of 11% by 2026. Brands like Sol de Janeiro have found success by appealing to Gen Z with gourmand scent mists designed for layering, a trend that gained traction between 2025 and 2026. Moreover, emotional resonance plays a significant role, as 80% of consumers now select perfumes based on their ability to enhance mood and well-being.

8. Seasonal and Emerging Trends

Winter Intensity and Wellness — Driven Scents Are Shaping 2026

Seasonal shifts are bringing fresh energy to fragrance preferences, with Winter 2026 spotlighting deeper, moodier scents. Light florals are stepping aside for "dark intensity" profiles, featuring bold notes like black florals, cocoa, saffron, and cardamom. These richer fragrances tap into a growing desire for scents that evoke emotion and individuality. Alongside this, nature-inspired experiences are gaining ground as more people gravitate toward grounding elements such as aged woods, balsam, herbal roots, and even biotech-inspired accords like petrichor to foster a connection with the natural world.

The market for "sensory nostalgia" is also booming, driven by sweet, comforting notes like caramel and buttery vanilla, with projections placing its value at $23 billion by 2026. Social media is amplifying these trends, with searches for floral fragrances soaring by 225% and "dark cologne" searches skyrocketing by 1,000%. Additionally, 65% of U.S. consumers are moving beyond single scents, opting instead to layer fragrances across body, hair, and personal care products for a more personalized experience.

Regional preferences continue to shape these trends, reflecting diverse cultural influences. For instance, Middle Eastern consumers remain loyal to oud-based luxury perfumes that highlight regional traditions. In contrast, Japanese buyers lean toward soft, understated scents. Meanwhile, clean-label, wellness-focused fragrances dominate in Germany, and in China, the growing middle class is driving demand for travel-friendly formats and Western-inspired scents.

"Winter fragrance will meet the demand for more inventive scent profiles, seizing the dual opportunity to position play as a new wellness pillar while meeting consumer demand for greater self-expression through scent." - Cosmetica Labs

These shifting consumer preferences are also shaping how brands approach regional markets. Limited-edition seasonal collections now account for 15% of luxury perfume sales. Brands are leveraging cultural moments like Lunar New Year and Diwali in the Asia — Pacific region by introducing exclusive packaging tailored to these celebrations. For example, in November 2025, Coty Inc. launched Chloé Rose Naturelle Intense - its first refillable perfume line - to meet the growing demand for eco-friendly packaging solutions.

2026 FRAGRANCE TRENDS

Conclusion

The perfume industry in 2026 is undergoing a transformation that extends far beyond simple market growth. With the global market valued at $82.38 billion and expected to reach $121.26 billion by 2031, growing at an annual rate of 8.04%, changing consumer preferences are reshaping everything from product design to how fragrances are sold. These shifts are redefining the industry landscape in significant ways.

Here are three key trends driving this evolution:

- Premium fragrances are leading the charge, with this segment holding 65.25% of the market share and growing at 8.45% annually. High-concentration formats are becoming increasingly popular, as explored earlier in this article.

- Digital innovation is transforming the buying experience, with tools like AI-powered scent profiling and virtual try-ons helping overcome the sensory limitations of online shopping. Online retail is poised to grow at a rate of 9.21% to 12.4% CAGR.

- Sustainability has become non-negotiable, with brands embracing refillable packaging and biotech ingredients to meet the expectations of 65% of luxury consumers who now prioritize eco-conscious options.

Regional trends also highlight where the perfume market is headed. Europe continues to lead with its heritage brands, while the Asia — Pacific region is emerging as the fastest-growing market, expanding at a 9.54% CAGR. Additionally, the unisex fragrance segment is experiencing rapid growth, with a 9.3% CAGR, as traditional gender lines in scent preferences blur. These developments are reshaping how consumers discover and engage with fragrances.

Scento’s proprietary data provides a closer look at these shifts. With 85,000+ active members, 1,000+ curated fragrances, and 75,000+ quiz completions (Scento internal data), the platform is uniquely positioned to track these trends in real time. The rise of personalized discovery, smaller packaging formats, and subscription models reflects the modern consumer’s desire for convenience and individuality.

The numbers tell a compelling story: the perfume industry is becoming more tailored, eco-conscious, and digitally forward, offering consumers unprecedented choice and control. Brands that embrace these changes will not only remain relevant but also thrive in this increasingly sophisticated market. Those that resist risk falling behind in a rapidly evolving landscape.

FAQs

How is Gen Z driving growth in the perfume industry?

Gen Z is shaking up the fragrance world by focusing on emotional connection and self-expression rather than traditional ideas of luxury. For them, perfumes aren’t just accessories - they’re tools for showcasing individuality. One popular trend among this group is scent-stacking, where they layer multiple fragrances to craft a signature, personal scent.

Social media platforms, especially TikTok, play a massive role in how this generation discovers and chooses scents. Fragrance shopping has become more interactive and trend-driven, with digital influencers and viral content shaping their decisions. Beyond aesthetics, Gen Z places a strong emphasis on sustainability, transparency, and inclusivity. They gravitate toward gender-neutral fragrances and ethically sourced ingredients, encouraging brands to rethink their approach to meet these expectations.

Interestingly, Gen Z is also spending more on fragrances than older generations, driving growth in the market. Their focus on digital trends and values-based consumption is not only reshaping the industry but also sparking fresh ideas and new directions for brands.

How is sustainability influencing the perfume market?

Sustainability is playing a growing role in the perfume industry, influencing both production methods and marketing strategies. Younger consumers, particularly millennials and Gen Z, are showing a strong preference for fragrances that highlight natural ingredients, eco-conscious packaging, and ethically sourced materials. This shift in priorities is reshaping how brands connect with their audience.

In response, many perfume companies are adopting practices aimed at reducing their environmental impact. From cutting carbon emissions to improving resource efficiency, these changes align with global environmental goals. Beyond the ecological benefits, such efforts help build trust and loyalty among consumers, positioning sustainability as a driving force behind innovation and progress in the fragrance world.

How is technology changing the way people buy perfume?

Technology is reshaping the way we shop for perfumes, making the experience more engaging, personalized, and convenient. Social media platforms like TikTok are playing a big role in driving purchasing decisions, with nearly half of consumers influenced by the content they encounter online. At the same time, e-commerce is thriving, with online perfume sales expected to grow from €3 billion today to over €5 billion by 2027.

Brands are leveraging artificial intelligence and data-driven tools to offer personalized recommendations and immersive digital experiences. These advancements allow shoppers to explore and choose fragrances without relying on physical samples. Additionally, the rise of subscription services and travel-sized options - often promoted online - is changing buying habits, offering more flexible and convenient ways to enjoy luxury scents. These tech-driven innovations are helping brands connect with younger, tech-savvy audiences while transforming how consumers discover and purchase their favorite fragrances.

By Sebastian Dobrincu, Founder & Industry Analyst at Scento

Perfume Production Statistics

Modern perfumery runs on a 70/30 split between synthetic aroma molecules and natural extracts — a ratio that has held steady since 2015 and shows no sign of inverting. The synthetic share is structural, not aesthetic: IFRA restrictions on naturals like oakmoss, treemoss, and certain animalic extracts narrowed the natural toolbox, while captive molecules — proprietary aromachemicals owned by Givaudan, Firmenich, IFF, and Symrise — became the differentiating raw materials of contemporary fine fragrance. Even niche houses marketed as 'natural-leaning' typically use a synthetic-natural blend; pure naturals are rarely commercially viable at the longevity and projection consumers expect.

European production concentrates in three hubs. Grasse, the historic capital, anchors natural-extract production — jasmine, rose, tuberose, lavender — and houses roughly half of France's fragrance manufacturing workforce. Versailles serves as the contract-manufacturing capital, where many prestige juices are produced under white-label agreements before being shipped to brand-specific bottling. Geneva is the corporate-and-creative hub, headquarters to the four major fragrance houses that supply most of the world's perfumers with raw materials and base accords.

Spain has emerged as the quiet production powerhouse: Scento's review of EU export data shows Spain accounting for approximately 27% of EU fragrance output by export value, driven by Puig's manufacturing footprint in Catalonia. Italy contributes specialised craft production from Florence, Milan, and Bologna; the UK retains a small but high-margin manufacturing presence. Total European fragrance manufacturing employment exceeds 90,000 people directly, with multiples of that figure in the indirect supply chain — glass flacon production, packaging, distribution, retail, and the long tail of perfumery education.

Production volume metrics underline how concentrated the industry is. Scento's analysis of European fragrance manufacturing output puts annual finished-juice production at approximately 1.4–1.5 billion units across all tiers. Roughly 60% of that volume traces back to fewer than fifty contract manufacturers, with the top ten producers — including Cosmétique Active International (L'Oréal), Albéa, COSMOGEN, and the Puig manufacturing arm — handling more than 35% of EU fragrance bottling alone. Glass flacon production runs almost entirely through six European glass houses (Verescence, Bormioli Luigi, Pochet, SGD Pharma, Stoelzle, and Heinz Glas), creating a structural bottleneck at the packaging layer that constrains how quickly any new prestige launch can scale beyond limited-edition rollouts.

Top Perfume Companies by Revenue 2026

Seven conglomerates dominate global prestige fragrance revenue in 2026. LVMH's Perfumes & Cosmetics division leads, anchored by Christian Dior, Guerlain, Givenchy, Maison Francis Kurkdjian, and Loewe. L'Oréal Luxe holds second on the strength of YSL Beauté, Lancôme, and a portfolio of licence-distributed houses including Maison Margiela Replica.

Coty Inc. — through its Coty Luxury division — controls Calvin Klein, Hugo Boss, Gucci, Burberry, and Tiffany & Co. fragrance licences. Estée Lauder Companies own Tom Ford Beauty, Aerin, and Le Labo (acquired 2014), giving them disproportionate niche exposure relative to their total revenue. Inter Parfums distributes Jimmy Choo, Coach, Lacoste, and a long tail of fashion-house licences. Puig — Spain's family-owned beauty conglomerate — owns Carolina Herrera, Paco Rabanne (now Rabanne), Jean Paul Gaultier, and Penhaligon's. Shiseido rounds out the top tier through its Narciso Rodriguez, Issey Miyake, and Serge Lutens portfolio.

The conglomerate-vs-niche split tells the more interesting story. Scento's order analysis shows the top seven conglomerates capture roughly 70% of European prestige fragrance revenue, but their growth rate sits at the category average of 4–5% annually. Independent niche houses — Creed (acquired by Kering in 2023), Byredo, Le Labo, Diptyque, Jo Malone London, Amouage, Xerjoff, Parfums de Marly — capture a smaller revenue base but compound at 8–11% annually. The acquisition pipeline reflects this: every conglomerate has either bought into niche or is actively scouting.

The acquisition history of the past decade reveals the strategic logic. Estée Lauder bought Le Labo (2014) and Frederic Malle (2014). Puig acquired Byredo (2022) and Penhaligon's. Kering brought Creed in-house in 2023 for an estimated $3.8 billion, the largest niche acquisition on record. L'Oréal absorbed Aesop in 2023. The pattern is consistent: conglomerates pay multiples of 10–15× revenue for established niche houses to acquire growth they cannot manufacture internally. The creative scarcity of niche — founder-led, narrative-driven, scarcity-priced — does not scale through conglomerate operating playbooks, which is why acquisition rather than organic-launch is the dominant entry path.

Perfume Market by Price Tier

Three price tiers structure the global perfume market, and they answer different commercial questions. The mass tier — fragrances priced $0–$49 — dominates by unit volume, accounting for roughly 65% of all perfume bottles sold worldwide. The premium tier — $50–$149 — captures the largest share of new buyers; this is the entry point most consumers cross when they graduate from mass to prestige. The luxury and ultra-luxury tier — $150+ — dominates by revenue despite representing a small minority of unit volume.

The split is starkest in Europe. Scento's review of regional revenue distribution shows the $150+ tier accounting for over 55% of total revenue across Western Europe, against approximately 35% of unit volume. The $0–$49 tier inverts: roughly 65% of unit volume against 18% of revenue. The middle tier ($50–$149) is the volatile zone — where direct-to-consumer brands, dupes, and indie houses compete for the consumer who is moving up but has not yet committed to luxury.

Decant economics break the price tier framework. A 2ml decant of a $300 luxury fragrance retails at roughly $5–$8, putting it in the mass tier by absolute price but in the luxury tier by per-millilitre cost. Scento's category exists precisely in this gap: it lets buyers experience the luxury tier without committing the luxury tier's full-bottle price. This is why the price-tier framework is increasingly inadequate for the 2026 market — the relevant question is no longer 'what tier did this fragrance launch in', but 'at what entry point can the consumer access it'. Browse perfume samples to see the per-millilitre economics in practice, or find your scent via the matching quiz.

Tier mobility — the rate at which buyers move up the price ladder — is the most-watched metric across the prestige industry. Scento's analysis of European purchase sequences shows the average buyer entering at the $50–$149 tier reaches the $150+ tier within 14–18 months when sampling-and-decant access is available. Buyers without that access typically take 3–4 years to make the same transition, if at all. The decant channel functions as a tier-mobility accelerant: it removes the financial commitment that historically gated luxury-tier trial, which is why luxury brands have moved from resisting the decant economy in 2018–2020 to actively partnering with regulated decant retailers from 2023 onward.

Gen Z Perfume Buying Statistics 2026

Gen Z buyers — born approximately 1997–2012 — are the most-researched fragrance cohort in the modern category, and the numbers explain why brands are reorienting their entire discovery funnel around them. Average annual fragrance spend among Gen Z buyers reached roughly $200–$220 in 2025–2026, up approximately 25% from millennials at the same age. Gen Z men in particular spend 35–40% more per order than millennial men did at equivalent life stage — the cohort effectively cleared the social stigma around male fragrance interest, and the spend reflects it.

Discovery channels skew sharply. Roughly 66% of Gen Z buyers report TikTok as the primary discovery vector for new fragrances; Instagram sits second at approximately 38%; YouTube reviewers third at 31%. The bricks-and-mortar perfume counter — historically the dominant first-encounter channel — drops to fifth or sixth place for this cohort. Niche fragrances perform disproportionately well in this discovery model: TikTok rewards distinctive, conversation-starting scents, which biases the cohort toward niche over designer at a higher rate than any prior generation.

Sample-and-decant adoption is the structural Gen Z signal. Scento's order data across 19 European markets shows Gen Z customers preferring 2ml and 5ml decants for initial trial, then converting to 30ml and 50ml bottles once a signature note family is identified. The discovery sequence — sample, decant, mid-size bottle, full bottle — is roughly four times more granular than the millennial-era pattern of go-to — Sephora-and-buy-100ml-blind. The cohort is more cautious with money and more confident with taste, and the decant economy is the natural product format for both. Browse women's fragrances, men's fragrances, or curated new arrivals.

Note preferences also diverge from prior cohorts in measurable ways. Scento's analysis of Gen Z order data identifies pistachio, ambroxan, iso-e-super, and the gourmand-vanilla family as outsized growth notes — frequently mentioned in TikTok-led discovery conversations and converting to actual purchase at 2–3× the rate of the broader catalog. Edible-perfume formulations (cherry, caramel, espresso, salted caramel) reportedly grew over 900% in social conversation between 2022 and 2025, validating the cohort's appetite for distinctive-and-conversational scent profiles. The structural takeaway is that Gen Z is not simply spending more on the same fragrances older cohorts buy — they are actively shaping which notes become commercially dominant in the prestige category.

Industry Employment & Manufacturing Footprint

The European fragrance industry directly employs over 90,000 people in manufacturing roles, with multiples of that figure across the indirect supply chain — glass flacon production, packaging design, perfumery education, distribution, retail, and the editorial-and-influencer ecosystem that increasingly drives discovery. France leads on direct manufacturing employment, with roughly 32,000 people in fragrance-related production roles concentrated in Grasse, Versailles, and the Île-de — France packaging cluster. Spain follows on the strength of Puig's Catalonia footprint and the long tail of contract manufacturers serving European licence-distributed houses.

Italy contributes specialised craft and artisan production, with significant employment around Florence, Milan, and Bologna; the UK sustains a smaller but high-margin manufacturing base around the Penhaligon's and Floris heritage clusters; Germany's contribution is concentrated in raw-material chemistry through Symrise. Switzerland's contribution is outsized relative to employment count: Geneva's four major fragrance houses (Givaudan, Firmenich, IFF, Symrise) employ roughly 15,000 people across global operations, but the creative output supplies the perfumers behind most of the world's prestige fragrances.

The downstream employment story is the more dynamic one. Scento's analysis of the European fragrance ecosystem suggests that retail, distribution, e-commerce operations, perfumery education, and the editorial-and-creator ecosystem account for an additional 250,000+ roles across Europe. The fastest-growing employment vector is the creator economy: dedicated fragrance reviewers on TikTok, Instagram, and YouTube now influence a non-trivial share of category discovery, and the indirect headcount of agencies, talent management, and creator-supply operations has roughly doubled since 2022.

Perfumery education itself has expanded as a discrete economic segment. The Institut Supérieur International du Parfum, de la Cosmétique et de l'Aromatique Alimentaire (ISIPCA) in Versailles, the Grasse Institute of Perfumery, and the newer programmes at Cinquième Sens and the Robertet Academy collectively enrol several thousand students annually. The talent pipeline matters strategically because the bottleneck on niche-launch volume is creative — there are only a limited number of trained perfumers capable of composing prestige-level juice, and the conglomerate–niche acquisition pattern competes with new niche launches for the same scarce creative output.

Counterfeit Perfume Statistics 2026

Counterfeit fragrances cost the legitimate European industry an estimated $3 billion in displaced annual revenue. Perfume ranks consistently among the top three product categories seized at EU borders by intellectual-property enforcement units; Scento's review of customs data shows fragrance shares fluctuating between 8–14% of total IP-related EU border seizures by value, depending on the year. Counterfeits cluster around the most-recognised prestige names — the iconic flacons of Chanel, Dior, YSL, Tom Ford, and Creed — because counterfeit economics depend on consumer recognition.

The distribution channels are well-mapped: low-trust online marketplaces, social-commerce listings, grey-import resellers, and unauthorised pop-up retail. Roughly 5–10% of fragrance products sold through unauthorised marketplaces are counterfeit, with the share rising sharply for products listed at 50–70% below typical retail. The counterfeit economy clusters geographically — production typically in China, Turkey, and the UAE; distribution often via Eastern European and Mediterranean entry points; consumer fulfilment increasingly via dropshipping models.

The countermeasures matter for legitimate buyers. Authorised retailers — including Creed, Tom Ford, Maison Francis Kurkdjian, Byredo, and Le Labo on Scento — operate within a verified supply chain that traces juice from manufacturer through distributor to consumer. The decant economy adds a useful authentication layer: when a sample is decanted from a verified full bottle by a regulated retailer, the chain-of-custody is short and traceable. Browse the full perfume catalog, the curated best-sellers, or perfume gifts; explore the notes index if a specific accord is the starting point.

Detection is harder than buyers expect. The most-common counterfeit indicators — misaligned print on the box, slightly mismatched bottle weight, batch codes that fail authentication — require side-by-side comparison or specialised tooling that the average consumer does not have. Scent itself is the least-reliable test: a competent counterfeit operation can match the top-and-mid notes well enough to pass casual sniffing, even though the dry-down typically diverges. The consumer-protection lesson is straightforward — buy from authorised channels with traceable supply chains, treat below-50% retail pricing as a red flag, and prefer the decant or sample channel for unfamiliar fragrances rather than discounted full-bottle listings on uncontrolled marketplaces.

This analysis is based on Scento's review of European fragrance industry data, October 2025 – April 2026. A detailed methodology is available to press on request at [email protected].